Venture Capital and Leverage Ratios

Understanding leverage is important, this is why you should care about it

Introduction to Rare Candy

Welcome to the inaugural edition of Rare Candy. I’m pretty excited to be writing this (and for you to be reading!).

I’ll keep this introduction short, because I know why you’re here.

Rare Candy is a monthly newsletter providing you with deep, insightful analysis about investing, venture capital and technology. It will almost certainly be quantitative and data-driven and hopefully, it will be novel analysis.

At times, it may also be about other things I’m interested in such as sports, cooking, pop culture, millennial dating, books, memes and more. But I’ll keep it relevant to venture and investing where I can.

If you’re interested in collaborating, please reach out to me here. I’d love to share some ideas and see how we can work together.

Like what you’ve read today? Coffee is getting expensive and I need it to keep writing.

Summary

Key Insights and Ask

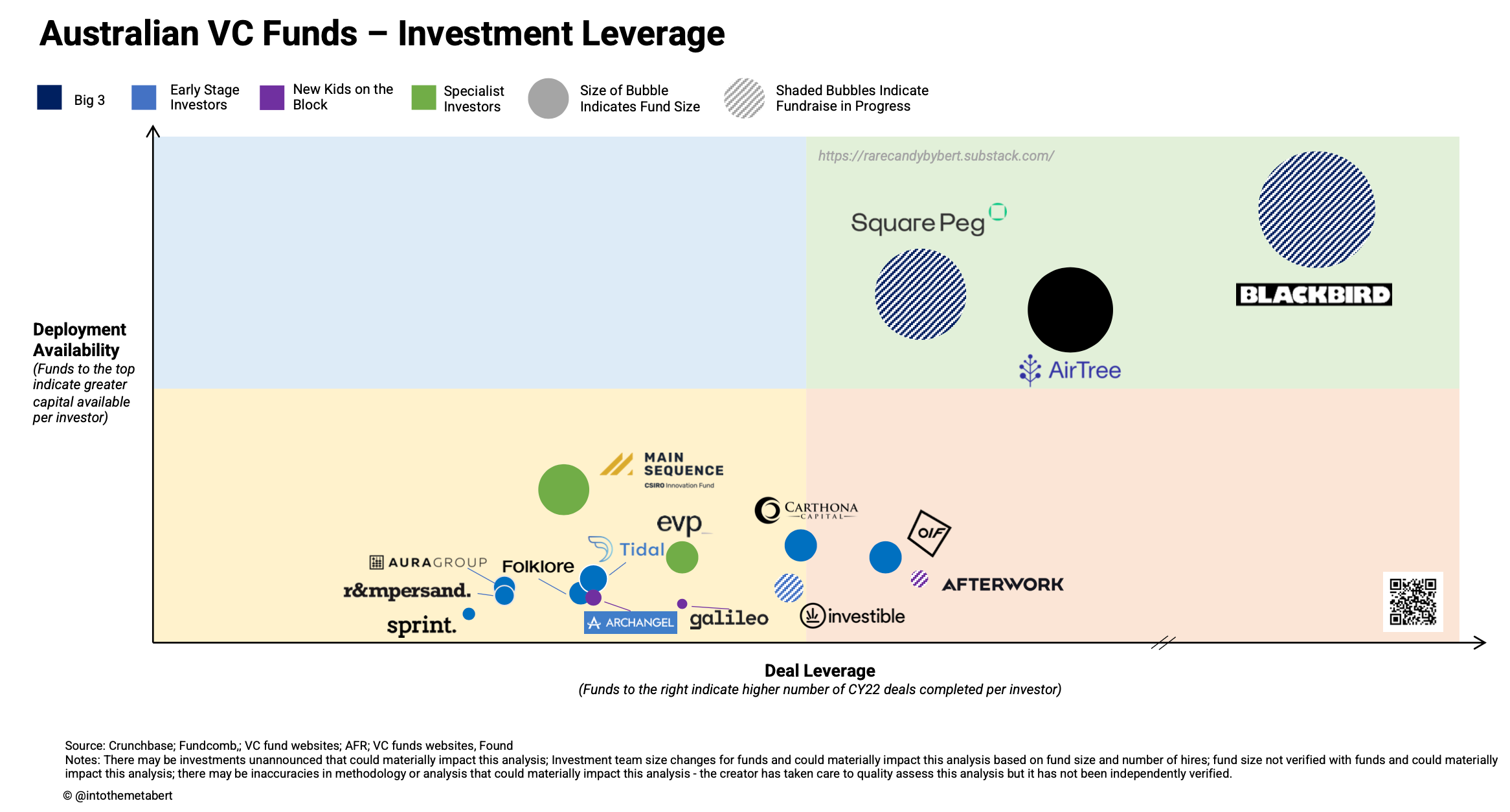

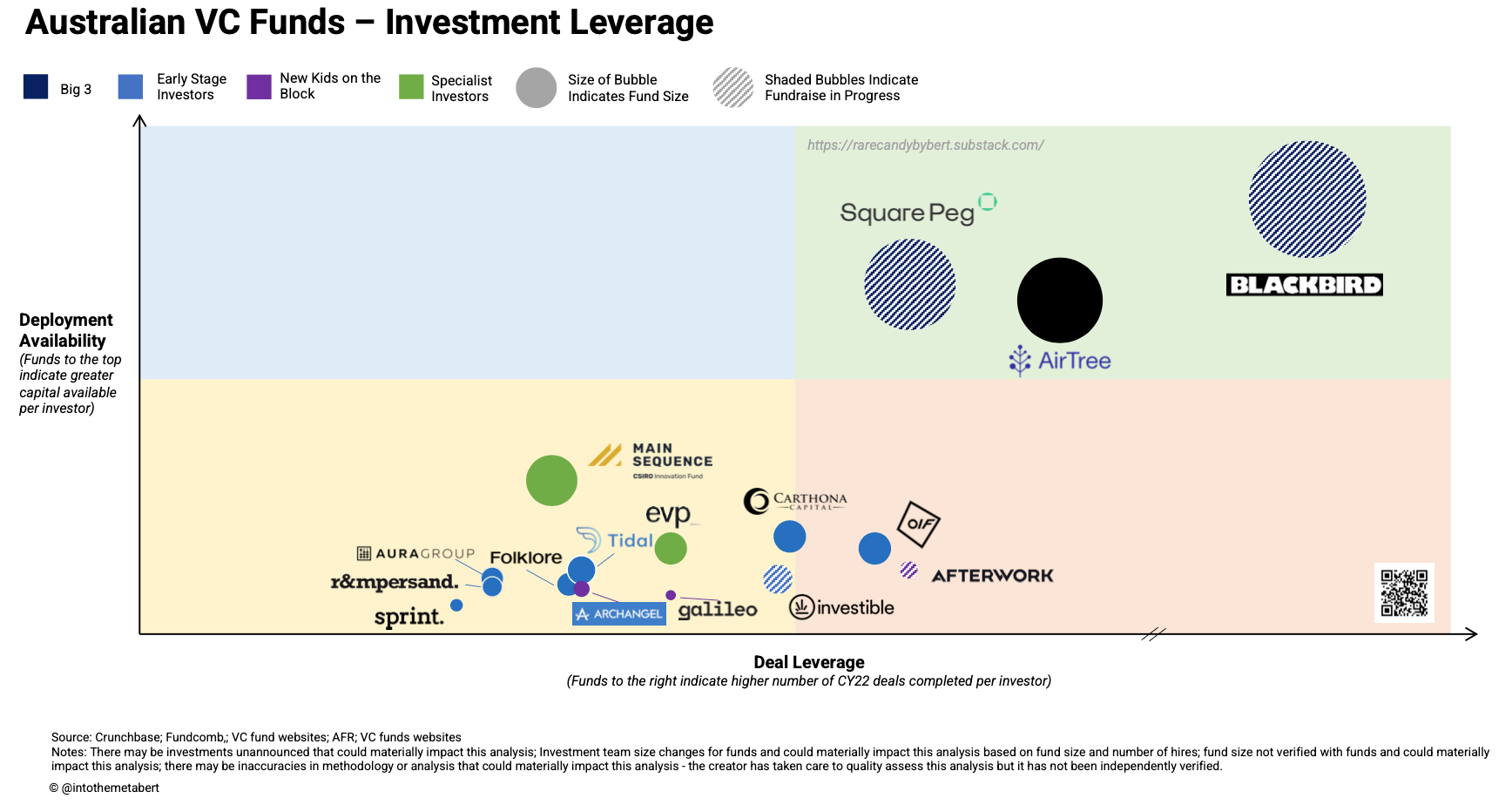

Just here for the chart? Here is what you need to know:

The ‘Big 3’ VC funds are in a league of their own - Square Peg, AirTree and Blackbird have incredible efficiency at both sourcing deals and deploying capital.

Differentiation in approach is working - Funds like AfterWork, EVP and Galileo are showing they can compete by differentiating their focus and their approach. More on this below.

Capital allocation strategy differs across funds - It’s still a power law game, but the game is played differently by funds.

My Ask: Reach out to me and provide me with updated data for my charts. This data won’t be shared with anyone else and it won’t be made public on this newsletter.

Note: Not every VC fund is included. This data requires a lot of manual input so I focused on a selection. Want to help with future analysis? Reach out!

I love investing. I’m addicted. I love ‘leveling up’ and learning about interesting asset classes like vinyls, whiskey, Pokemon cards and more. That's why I've been reading Alts. Stefan and Wyatt write deep analysis on alternative assets and you get to reap the rewards.

Join 50,000 others and see what you’ve been missing. Subscribe to Alts for free.

Introduction to Leverage Models

Leverage models are a way to understand how work gets delivered by organisations. Commonly used in professional services firms (law, consulting, banking etc), they help you understand the mix of ‘grinders’ (the analysts / associates like yours truly who ‘do’ the work), the ‘minders’ who babysit the grinders and the ‘finders’ who win work for the minders and grinders to deliver.

I’ve applied this to understand three ratios across a selection of Australian VC funds to understand how work (or capital) gets delivered:

Investment Team Leverage - Ratio of Partners to other investors (analysts, associates, managers, principals and directors). As leverage increases, Partners are freed to do other things like fundraise and meet LPs, thesis development, advise Boards and founders and grow their twitter following and less time ‘grinding’.

Deployment Availability - Ratio of funds available to deploy (or funds being raised to deploy) per investors at a fund. This doesn’t mean every investors get free reign to deploy that capital (although some funds do operate this way) but provides an indicative and directional view of how funds staff and structure their investment teams based on their fund size.

Deal Leverage - Ratio of the investments closed this calendar year per investors at a fund. You could say it’s an indicative and directional view of the number of deals each investor makes. While in practice this isn’t really true as funds have their own decision making processes and governance structures, it’s a binary way to think about investments and investment teams. If you assume that 1 in every 100 startup gets venture backed, you could even use it as a proxy for deal sourcing and coverage - more deals you see, the more deals get done.

Why is this important?

If you’re an investor at a VC fund, I’d be shocked if you hadn’t done this analysis internally already on your own fund, or another fund. Understanding these ratios provides investors with foresight on internal budgeting, fund and investor performance. Understanding the staffing requirement to deploy the fund you’ve raised by using these ratios is particularly useful, but even more useful is understanding the staffing requirement required to source and see the right deals (some funds have found a cheat code to sourcing and have seeded other funds for coverage and flow. If you want to seed a fund, reach out to me 💰).

These ratio help with answering two key questions for investors: Based on our investment team size, are we:

Investing at the right rate (amount, quantity of capital etc)?

Seeing the right volume of deals?

Why am I doing this analysis?

The short answer is that I love doing this type analysis, I love uncovering this insight and I really love bubble charts. Maybe it’s Stockholm Syndrome from being an ex-strategy consultant?

The serious answer is that I aspire to become a great venture investor and part of this journey for me is truly understanding this industry and its opaque nuances. Aptly named, this newsletter is about my journey to the Elite Four, and by learning what I can about the other ‘Trainers’ and ‘Gyms’ in this industry, it’ll help me get better at the craft of venture.

Investment Team Leverage

This is what the current investment team leverage looks like across the VC landscape. Higher leverage implies a greater ratio of non-Partner investors to Partners in a fund. As a side note - I don’t buy the notion that founders need to be speaking to a Partner straight away. Analysts and associates can become incredible advocates for founders (they’re generally young and hungry to prove themselves).

As funds scale and grow in size, they build higher leverage models to support growth. Blackbird are looking to raise a fund could range in the $1-1.3bn+ range and their leverage model likely reflects that. Smaller funds are naturally top heavy given they have smaller (in aggregate) dollars to pay for salaries, leading to leaner teams that are mainly Partners.

The outlier here is Square Peg which has the lowest leverage of any of the Big 3 and almost lower than most funds on this chart.

There is a lot of you can imply or speculate on regarding this chart - it’s not that interesting to me in isolation so let’s move onto the meatier analysis.

(Maybe a fund with higher leverage will see this chart and promote someone to Partner just to reduce leverage the next time I publish it).

Analysing VC Leverage Ratios

Across these funds, there is $3.7bn in funds raised (or to be raised) and ~120 investors.

Square Peg, AirTree and Blackbird are truly in a league of their own when it comes to venture in Australia. These funds have shown strong ability to get deals across the line and haven’t slowed activity despite the market conditions. It’s worth calling out that these funds also have 2-3x the size of investment team than other funds and have managed to close more deals per investor than the other funds on this chart. They’ve grown in scale and efficiency, which was a surprise to me as my initial hypothesis was the inverse but it shows the strength of these funds.

Up and to the right is Blackbird. If you believe the hypothesis that funds increase their deal leverage as they scale (i.e. more people = more deals), it makes sense that they’re firmly in the top quadrant. I’ve even cut this chart with axis breaks because they were skewing it too far to the right. They’re raising their latest fund at the moment and I’m unsure whether they’ll hire another crop of investors so I’m sure this positioning could change, but again, if you believe in the above hypothesis, they might continue to shoot off to the right.

AirTree and Square Peg are closer in positioning - they have similar fund sizes, investment team sizes and have closed a similar amount of investments this calendar year. Two calls outs on this:

AirTree have recently hired two new investors (and an investment research manager), all three of which are included as part of this analysis. If we take them out, AirTree move further to the right and much more closely aligned to Blackbird. I’d be suprised if these investors have closed deals in between the time they joined AirTree and this article being written seeing as it’s relatively recent but only AirTree can tell me that.

Square Peg only has 5 investors who are focused on Australia. This puts their AU presence at half the size of these other funds. If you assume they’re sourcing deals at the same volume in aggregate as both AirTree and Blackbird, this implies incredible sourcing coverage and efficency.

There’s more I want to write on these three but they’re better placed below in the Geographical Coverage and Domain Coverage write-up. And besides, I have to keep you reading.

Let’s take them out for now, because they're skewing the chart…

We start to get some really interesting insights. In the orange quadrant, there are a few interesting funds that I want to call out specifically because they’ve all differentiated themselves outside of the normal ‘early stage investor’.

AfterWork Ventures has differentiated itself from other funds and leverages (see what I did there?) a community-powered approach to investing.a AfterWork is proving that this model is working - if you believe that deal leverage could be used as a proxy for deal coverage (the hypothesis above), then it’s apparent that their community-powered approach is a unique superpower that gives them similar deal leverage as the Big 3 but without the team size.

OIF and Carthona are interesting funds too and differentiated in a different way. Both are funds that don’t have ‘investing-adjacent’ pursuits in the way some other funds do but both funds boast high deal leverage and their investment teams are below the average size of VC funds in the country.

Investible is an interesting fund because they have broad geographical coverage and broad domain coverage. They play across SEA and have multiple fund types (i.e. early stage fund, climate focused fund) and I think this lends itself to getting more deals done, partly due to the fact they’re probably just seeing a greater volume of deals. More on this below.

EVP is another really interesting fund because they predominately invest in B2B SaaS (btw EVP if you’re reading this, I’ve invested in two B2B SaaS companies that you should definitely mark up for me, reach out!). They’re likely seeing almost every B2B SaaS business in AU and NZ and can win those deals given their status and expertise in the space.

Lastly, Galileo is a new fund that invests only in first-time founders and they aim to be the first cheque in those companies. This proposition is proving to be attractive for founders and they’ve co-invested alongside some great US funds including a16z and Insight Venture Partners.

Thematically, these funds have differentiated themselves either through their approach to sourcing, investing activities, or which segments of the market they invest in and it’s proving very well. As the VC space becomes more saturated, this differentiation will continue to be the key to their success and the success of new funds.

Lastly, the blue quadrant is really interesting to me. Main Sequence Ventures is a deep-tech investor and there’s very few deep tech start-ups in Australia (watch this space because I’m sizing this market and will publish my results in the coming months). Given that the ‘top of funnel’ is smaller in aggregate for MSV, their positioning makes sense here. It would be interesting to do this analysis but for deep tech focused funds only!

Geographical Leverage

Geographical leverage (or coverage) is an interesting overlay on this analysis. The majority of VC funds in Australia invest in AU / NZ founders and by nature of this, the majority of those founders are located in AU or NZ. This isn’t really insight at all.

The real insight (in my mind) is thinking about these investment teams, their coverage and comparing how these teams are structured.

Square Peg has 5 investors who cover Australia and the rest of their team covers South-East Asia (SEA) and Israel. Most VC funds have 5+ investors covering Australia, some even more so. To me, this implies that Square Peg are exceptional at sourcing because they can cover the same landmass as other funds but with fewer people. This isn’t necessarily true though because I don’t know if they see every deal in the country but it leads me to think about diminishing returns regarding sourcing effectiveness as you add new investors to an investment team unless you can tap into ‘alpha’ in some way. Something that could be true though - if you increase the diversity of your investment team as you increase size, you’re likely to see more deals. People of the same background will undoubtedly end up sourcing the same deals.

Aura is another interesting call out here - they have 6 investors who cover AU, NZ and SEA. Once again, this implies that Aura is exceptional at sourcing if they can effectively cover the region with this size of an investment team. They’re an early stage investor so their ‘market size’ is as large as it gets in venture.

Lastly, Investible has a presence in SEA with an office in Singapore but it looks like they have one dedicated investor in the region, supported by two investors based in Australia. They’ve investing across the region including Singapore, Indonesia and the Philippines which shows that they’ve got the ability to source across borders and even if it’s a lean team.

One last thing on this point - don’t read this as the AU based funds only invest in AU or NZ. Tidal Ventures has a presence in NYC and has invested in US companies. AfterWork just announced an investment in a SEA based company. Someone I lived with at college just got backed by a Big 3 fund and they weren’t even in the country (or had any connections with Australian VCs).

Domain Leverage

The last topic I want to cover in this article is Domain Leverage. I’ll be short here because this newsletter is already getting too long.

VCs invest in a range of segments and industries which means they need to effectively source and diligence these opportunities. This is hard. Diligence on a B2B SaaS startup is very different to a regulated MedTech startup and this again is very different to a Web3 startup. Sourcing is the same.

As funds grow in size, they need to find new areas of investment to deploy their cash into and part of their leverage models needs to account for these domains. Some examples here to show how domain leverage is playing out in practice. AirTree has a dedicated Web3 investor and Blackbird has a Scientist-in-Residence.

As we discussed above, some funds have specific domain mandates. EVP invests predominantly in SaaS. Main Sequences invests only in deep tech.

You can take this model to an extreme at generalist funds too - a16z has Partners who only focus on one segment or vertical. This enables them to source effectively and diligence effectively as they have domain experts who have cultivated a ‘halo’ effect in these verticals.

Will we get to that extreme in Australia? I’m not sure - the market might be too small for funds to be doing this consistently across the board, but differentiation is key to playing and winning in this game. I don’t think any new funds can be a ‘generalist early stage investor’ without genuinely having a differentiator, the landscape is becoming too competitive.

Limitations

This is point in time analysis made with unverified data points. You’ve probably noticed I’ve made assertions and conclusions and then followed up with ‘this isn’t necessarily true’. The difficulty of private markets is that data is scarce and fragmented, meaning analysis like this is hard to do without verified data.

Final Thoughts on Leverage Models

Leverage models in this space are super interesting because it exposes differences in fund structure and capital allocation strategy. a16z in the US fuctions almost like a consulting firm with its leverage model and the full-stack of services it offers to portfolio companies. Only bigger funds can compete in this way so for smaller funds, they’ll need to shift the other direction and continue to differentiate in novel and exciting ways in order to compete in this ecosystem.

This was a lengthy article, thank you for reading if you’ve made it this far. Did you find it useful? Let me know by sending me a message or sliding into my Twitter DMs.

What’s Next?

I’ll be releasing interesting analysis every month on investing, venture capital and technology.

I’d love to hear from you if there was something that reasonated in this article or if you have feedback for me. Shoot me a message, DM me on Twitter, add me on Linkedin, or even UberEats me some pizza.

If you’re interested in collaborating, please reach out to me here.

Reading, Cooking, Sports and More

As promised:

Reading - I finished reading Before the Coffee Gets Cold by Toshikazu Kawaguchi. If you’re into magical realism, I highly recommend it.

Cooking - Carbonara with speck is a game-changer, it crisps better than guanciale and has a more intense flavour.

Sports - I’m 4-1 (3rd of 12) in my Fantasy NFL league, taking a real money ball approach and barely watching game, only stats.

Life - After almost 5 years of living with one of my best friends, I’ve moved into my own place. It’s also right next to the office of a VC fund. Classic.

About Me

I’m Albert, I’m a technology investor and strategist. I grew up in Darwin, studied Chemistry and Law at the ANU in Canberra (with a brief stint in North Carolina at Chapel Hill), and moved to Sydney in 2018.

I started my career as a strategy consultant and left consulting to become an early employee at a venture-backed SaaS startup.

Now you can find me at Astral Ventures, on Twitter and on a tennis court or at a bouldering gym. In my free time, I co-host an investing podcast called Fresh Capital and now I write this newsletter.